Free Security Agreement Template

A Security Agreement is a legal document that establishes a lender’s rights to a borrower’s collateral in case of loan default. It outlines the loan terms, collateral description, and enforcement rights.

Each day has its dose of unpredictability, which can affect even the best-planned day. As we go through the day, we may occasionally face unforeseen financial difficulties due to the unpredictability of life. A Payment Plan Agreement, therefore, serves as a crucial lifeline—a break of fresh air—in these circumstances, giving people and businesses a planned and practical approach to offsetting debts and repaying borrowed funds either on a personal or corporate level

A Payment Plan Agreement is a legal contract that spells out how a debtor will reimburse or pay back a creditor. A creditor can establish a payment plan agreement to facilitate the debtor’s repayments and increase the likelihood that the whole amount of the debt will be repaid completely.

A Payment Plan Agreement is a legally binding contract between a debtor (the party liable for payment) and a creditor (the institution owed cash) that creates a schedule on how the loan will be repaid. This contract outlines the agreement and schedule for paying back a debt/loan or carrying out a financial commitment over a predetermined time frame. It gives debtors a structured substitute for a one-time payment, making it easier to manage their money.

A payment plan can also be utilized as a method of making a debt settlement to another party for goods or services that were received in exchange for money owed. The terms that both parties have agreed to are outlined in the detailed plan. It benefits borrowers who can’t afford to pay the entire price for products or services simultaneously or at the same time.

Payment Plan Agreements are extremely important to both parties, both on a personal and corporate level, for the following reasons: These reasons are briefly explained in clearer details

It serves as a means to resolve debts legally. Payment plan agreements provide debtors with a realistic and sustainable way to pay off their debts without incurring extra charges that could arise from non-payment of debts and also relieve them of the pressure of making large, lump-sum repayments. For example, a logistic company that deals with heavy-duty trucks for transportation can increase its fleet of trucks because it may establish a payment plan for the purchase of the trucks, which is capital intensive and could affect its working capital for the day-to-day running of the business if they were to pay at once.

Creditors are assured of a full refund: A firm commitment from the debtor lowers the risk of default, which benefits creditors. A productive commercial relationship may be maintained with the help of this organized strategy.

It offers legal protection: The agreement offers further protection for both parties by providing a legal structure that makes it enforceable in court if the debtor violates the provisions.

It promotes financial flexibility: Payment schedules can be altered to suit the debtor’s resources better, guaranteeing that payments are manageable and inexpensive.

Interest rates for payment plans can have a big impact on how much you end up paying over time. When you spread payments out over months or years, lenders often charge interest as the cost of borrowing. The interest rate is essentially a percentage of the outstanding balance that you pay back in addition to the principal amount.

For example, if you’re buying a car or financing a purchase with a 5% interest rate over a year, you’re paying 5% of the loan amount in extra charges. The lower the interest rate, the better it is for your wallet, because you’ll pay less over time. However, high-interest rates can add up quickly, making your payments more expensive in the long run.

Some payment plans offer 0% interest for a certain period, which can be a great deal if you can pay off the balance before the promotion ends. It’s always important to read the fine print and calculate how much you’ll owe in total, not just the monthly payment, to make sure it fits your budget.

The following are the steps for creating a payment plan:

Step 1: Describe Your Options

Meet with the borrower to discuss your alternatives for a payment schedule. Although some borrowers prefer to extend the payment duration, others might wish to pay off the loan as fast as feasible with fewer installments. To find a reasonable, equitable payment procedure, the creditor and debtor should discuss payment possibilities. The terms offered are frequently influenced by the kind of balance the debtor owes. It is advised that the creditor takes an interest in the balance, except the payment plan is an amicable arrangement between people who are familiar with each other.

Step 2: Complete the Agreement

With the borrower, go over each section and clause in detail. Make sure they are aware of and accept the conditions. Sign the document as the creditor and have the borrower sign it to complete the transaction. Additional Terms and conditions may be incorporated to include new provisions or details. The name of the additional documents (together with the page number) should be provided in a section if the creditor wishes to add an addendum or disclosure to the contract.

Step 3: Sign it

The signatures of the creditor and debtor are required to complete the agreement. If there will be a co-signer, they must also sign the paper. The parties must print their names legibly and include the date (mm/dd/yyyy) on which they signed the agreement.

Step 4: Start receiving payments

You can begin getting payments using the chosen payment mode once the payment plan arrangement has been commenced. Most payment plans demand the debtor to submit banking or credit card details to implement automated payments. Setting up automatic payments increases consistency and decreases the work required to get payments, so doing so is highly advised. If auto payments are not configured, the debtor will be required to make regular payments in accordance with the terms of the arrangement. You can discharge the borrower as a debtor after they successfully complete the agreed-upon payment period and make all required payments on schedule.

Although various creditors will draft different payment plan agreements, you should make sure to incorporate the following:

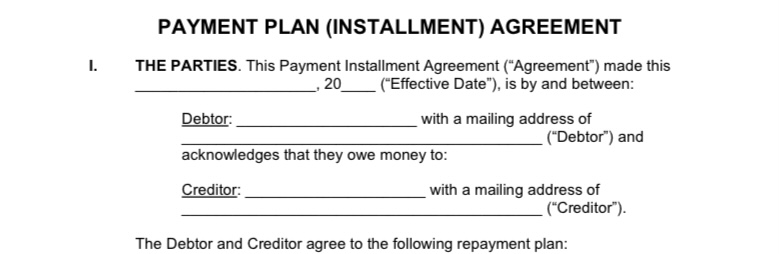

1. Date and Details of the Parties: First, fill in the date the agreement was made.

Then, specify the debtor and creditors’ names and mailing addresses. By providing this data, you can ensure that both parties are identified.

2. Total Debt: A payment plan agreement’s main objective is to repay the lender in full. You must specify the purpose of the loan and the total amount owed in the contract.

3. Start and End Dates: When drafting a payment plan agreement, it’s crucial to specify when the entire loan must be paid off. Make sure to specify the beginning and ending dates of the contract.

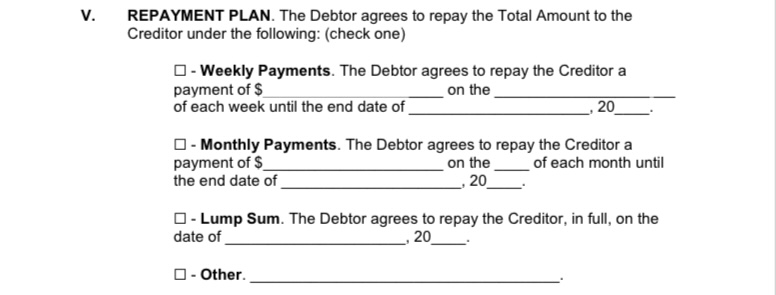

4. Payment Procedure: You must take the payment mode and the frequency of payments into account when drafting a payment arrangement. Will the borrower make one large payment, or will they make payments over time? If you opt for frequent payments, you must choose how often and when they will be made. You must also agree on the mode of payment.

5. Additional Terms: When drafting your payment plan contract, you should also take into account extra provisions like potential revisions, legal costs, indemnity, and an acceleration clause if the borrower is unable to make payments. If the creditor so chooses, they may insert any further terms and conditions here.

6. Signatures: Without a written contract from the lender and the borrower, your payment plan agreement will not be enforceable. Signing the document is formal evidence that all parties have agreed to its conditions. The debtor must print their name, sign it, and fill in the date (mm/dd/yyyy) on which they signed the contract. The same procedures outlined above must be followed by the creditor. Also, the same procedures outlined above must be followed if a co-signer is involved.

1. Explicit and Transparent Communication: Maintain open lines of communication with the debtor to handle any issues or modifications that might affect the payment plan.

2. Documentation: Maintain complete documentation of all payments, letters, and the signed contract.

3. Flexibility: Be prepared to make fair modifications to the payment schedule if the debtor has unforeseen financial difficulties.

4. Legal Evaluation: It is advised to have a lawyer evaluate the payment plan agreement, to make sure the Payment Plan Agreement is valid and enforceable,

A well-written Payment Plan Agreement is a strong financial instrument that enables people and enterprises to handle financial difficulties while retaining openness and legal protection. Both creditors and debtors can obtain financial strength and peace of mind in an often unpredictable financial environment by comprehending its importance, following the right procedures for creation, and adopting best practices.

It’s simple to base your agreement for payment plans on emails, messages, or spoken exchanges. It is possible to view these exchanges as an agreement; however, a signed contract offers you more protection and obvious evidence of everyone’s consent.

How Can I End a Payment Agreement?

A payment contract may be canceled, just like any other contract, if:

a. The debtor returns all money to the creditor.

b. Any party violates the terms of the agreement.

c. To terminate the agreement, all parties willingly agree.

Although it’s good, having a witness present is not legally required when signing a payment plan agreement.